What Is An Experience Modification Rate - Understanding the Difference Between Experience Mod and ... / The differences are reflected by an experience rating modification (mod), based on individual payroll and loss. An employers' experience modification rate refers the factor calculated from actual loss experience amd used to adjust an the businesses manual premiums (higher or lower) based on the businesses loss experience relative to the average underlying manual premiums. This means a good experience mod rate is anything below a 1.0 rating. The emr is a metric that insurers use to calculate the premium; Emr, or experience modification rating is a calculation used by insurance firms to price the cost of workers' compensation premiums. Your experience modification rate is derived or 'calculated' from your claims history.

What is experience modification rate (emr)? An employer with average experience has a modifier of 1.0 and would pay the manual premium. It takes into account the number of claims/injuries a company has had in the past, and their corresponding costs. What is an experience modification rate (emr)? Your experience modification rate is derived or 'calculated' from your claims history.

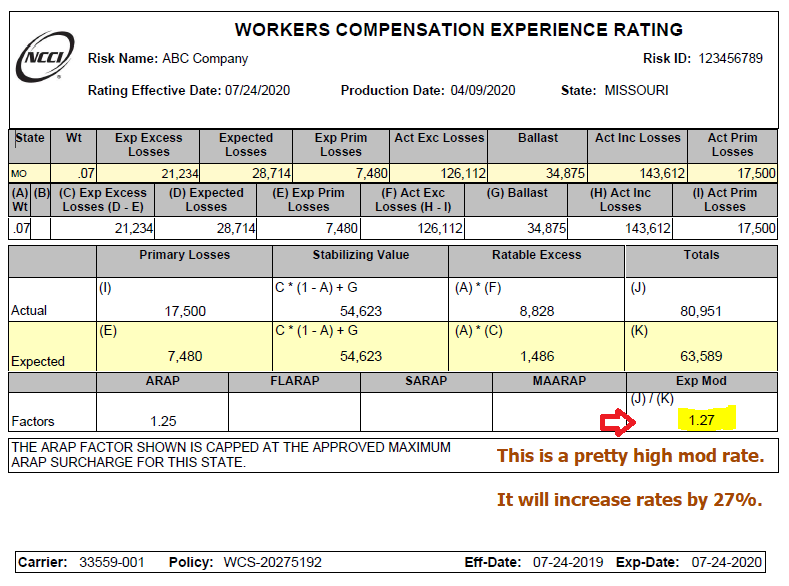

Experience Modification Rate - Emod, X-Mod, EMR Rating from www.workerscompensationshop.com An experience mod rate of 1.0 is considered the industry average for your business class. It takes into account the number of claims/injuries a company has had in the past, and their corresponding costs. Your emr basically states one of three things: So… how do these insurance agents calculate your experience modification rate? What is experience modification rate (emr)? The arap factor is calculated using the same components as the experience rating formula, but the arap formula relies more on total losses than primary losses. Do you understand what it is and how it impacts your premiums? Your experience modification rate is derived or 'calculated' from your claims history.

What is experience modification rate (emr)?

When applied to the manual premium, the experience modification produces a premium that is more representative of the actual loss experience of an insured. The lower the emr of your business, the lower your worker compensation insurance premiums will be. Your experience modification rate is derived or 'calculated' from your claims history. Your emr basically states one of three things: The rating reflects a variety lagging indicators, such as injury costs or claim history, and offers a prediction of future risk. Once the wcirb determines a business is eligible for experience rating its experience modification is calculated by comparing the actual losses to the expected losses. The experience modification rate, is a numeric representation of a business's claims history and safety record as compared to other businesses in the same industry within the same state. Employers with poorer loss experience would have modifiers greater than 1.00 and would pay more. An emr or experience modification rating (also called a mod rating or factor) is used to price workers' compensation insurance premiums. So… how do these insurance agents calculate your experience modification rate? It is a factor that compares your business' losses with other businesses in the same classification, and has the ability to increase or decrease your premium cost. It then compares the expected losses with those actual losses incurred over what's known as an experience period, usually a three year period of time, to develop the experience modification rate. An experience modification rate of 1.0 is the benchmark average.

Experience rating is typically based on the three years prior to the most recent expired policy period. The default average emr is 1.0 and the insurer uses this as a guide to assess your company's risk and calculate your premiums. The experience mod rate, or emr, is an important component of your company's workers' compensation program. What is an experience modification rate (emr)? An experience modification rate (emr) has a significant impact on the worker's compensation insurance premium of a business.

The Basics of Your Experience Modification Factor ... from www.emcins.com An employer with average experience has a modifier of 1.0 and would pay the manual premium. What is a 'normal' experience modification rate? The experience modification rate, emr or the emr rating, is a rating factor applied to all experience rated workers compensation policies. Emr, or experience modification rating is a calculation used by insurance firms to price the cost of workers' compensation premiums. Your company is riskier than average (emr > 1.00—results in a higher premium). The experience modification rate (emr) is a tool used by the u.s. An experience modification rate of 1.0 is the benchmark average. An emr or experience modification rating (also called a mod rating or factor) is used to price workers' compensation insurance premiums.

When applied to the manual premium, the experience modification produces a premium that is more representative of the actual loss experience of an insured.

The experience modification rate (emr) is a tool used by the u.s. What is an experience modification rating? The experience mod rate, or emr, is an important component of your company's workers' compensation program. Your company is riskier than average (emr > 1.00—results in a higher premium). What is a 'normal' experience modification rate? Do you understand what it is and how it impacts your premiums? Your experience modification rate is derived or 'calculated' from your claims history. You can verify that the emr, emod or xmod used on your policy is accurate through a experience modification rate review. The lower the emr of your business, the lower your worker compensation insurance premiums will be. A 1.0 experience modification rate means you are on par with your peers, and achieving the normal or expected safety outcomes of a company of your size in your industry. The rating reflects a variety lagging indicators, such as injury costs or claim history, and offers a prediction of future risk. An employers' experience modification rate refers the factor calculated from actual loss experience amd used to adjust an the businesses manual premiums (higher or lower) based on the businesses loss experience relative to the average underlying manual premiums. The differences are reflected by an experience rating modification (mod), based on individual payroll and loss

When applied to the manual premium, the experience modification produces a premium that is more representative of the actual loss experience of an insured. Arap applies only to employers that are in the assigned risk plan, are subject to experience rating and have an experience modification greater than or equal to 1.01. Emr is a number used by insurance companies to measure both past costs of injuries and future chances of risk. This means a good experience mod rate is anything below a 1.0 rating. It takes into account the number of claims/injuries a company has had in the past and their corresponding costs.

Blog | Blueprint Solutions from blueprintsolutions.us Insurance companies use the experience modification rate (emr) to establish future risk and set your company's premiums. It does this by comparing the experience of individual employers with the average employer in the same classification. This means a good experience mod rate is anything below a 1.0 rating. Your emr basically states one of three things: Your company is riskier than average (emr > 1.00—results in a higher premium). The experience modification rate, is a numeric representation of a business's claims history and safety record as compared to other businesses in the same industry within the same state. It takes into account the number of claims/injuries a company has had in the past, and their corresponding costs. A high experience mod will increase your annual insurance.

Recall your experience modification rate (or emr) is what's used by your insurance company to evaluate and measure risk they are taking on by having you as a client.

It then compares the expected losses with those actual losses incurred over what's known as an experience period, usually a three year period of time, to develop the experience modification rate. An emr or experience modification rating (also called a mod rating or factor) is used to price workers' compensation insurance premiums. Think of it like your credit score or car driving history, where third parties consider your history as an indication of future risk. The arap factor is calculated using the same components as the experience rating formula, but the arap formula relies more on total losses than primary losses. Emr, or experience modification rating is a calculation used by insurance firms to price the cost of workers' compensation premiums. You can verify that the emr, emod or xmod used on your policy is accurate through a experience modification rate review. How an experience rating is used an experience modifier is the adjustment of annual premium. What is an experience modification rate (emr)? The experience modification rate, emr or the emr rating, is a rating factor applied to all experience rated workers compensation policies. The lower the experience mod of your business, the lower your worker compensation insurance premiums will be. The lower the emr of your business, the lower your worker compensation insurance premiums will be. Recall your experience modification rate (or emr) is what's used by your insurance company to evaluate and measure risk they are taking on by having you as a client. Approximately 90 percent of workers' compensation premium dollars come from experience rated policies.